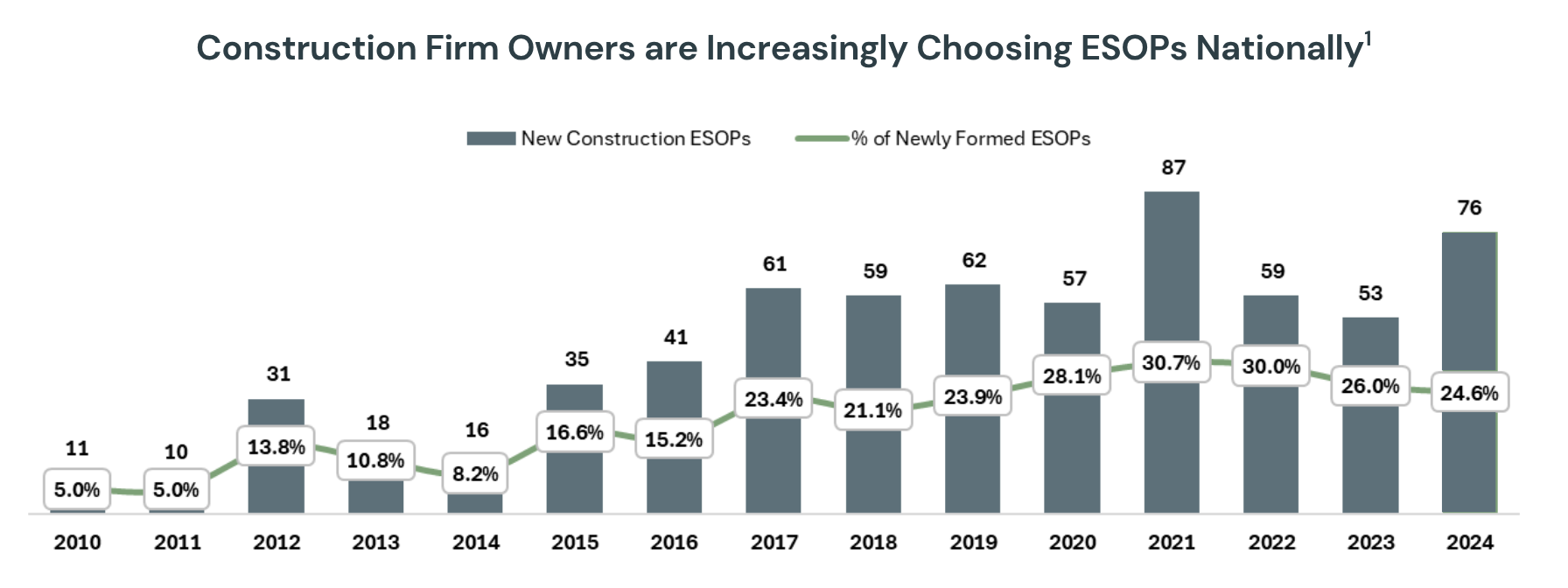

ESOPs: The Emerging Ownership Model for the Construction Industry

“Pursuing an ESOP was a natural choice for our company. We wanted to ensure our founder’s legacy lived on while preserving the culture and reputation that set us apart. Our accounting firm introduced us to BaseRock Partners, and from day one, they instilled confidence in us. Their deep expertise and ability to clearly outline each step of the process made all the difference. The BaseRock team was with us every step of the way; educating, advising, and ensuring we had everything in place to achieve a successful outcome. Their professionalism and strategic guidance were invaluable. We couldn’t be more pleased with our experience and would highly recommend BaseRock to any company considering an ESOP.”

“BaseRock Partners provided exceptional insight and advice as we navigated a very difficult decision-making process,” said Dick Ghilotti, Founder, Ghilotti Construction Company, one of the nation’s largest heavy civil construction firms. “Their leadership, market knowledge, and financial acumen were critically important to our owners and executive team. BaseRock will continue to be trusted advisors to our firm as we enter our next 100 years as an employee-owned company.”

“At Brix Paving Northwest, we believe in the incredible talent and dedication of our team. That’s why we decided to sell the company to our employees through an ESOP. They have contributed so much to our success, and now they get to write the next chapter,” said Billy Stimpson, President of Brix. “We’re grateful to BaseRock Partners for partnering with us on this process. We couldn’t have done it without their expertise. Their reputation as a leader in this field is well-deserved.

“BaseRock Partners came highly recommended to us within the construction industry, and their reputation as a leader in this field is well-deserved,” said Doug McAninch, owner of McAninch Corporation. Their guidance and expertise were instrumental in helping us navigate the complex process of transitioning to an ESOP. BaseRock not only provided valuable insight but also led us with precision through each step of the journey. We couldn’t have asked for a more capable partner during this pivotal time for McAninch Corporation.”